Dollarization and Foreign Shocks in Latin America

Dollarization eliminates the capacity to implement monetary policy freely, a move that critics argue leaves a country vulnerable to nominal foreign shocks. Detractors contend that relinquishing a central bank's ability to mitigate the impact of such shocks is ill-advised. This criticism, however, encounters two issues: one theoretical and the other empirical.

Theoretical limitations

In theory, a central bank could adapt its monetary policy in the face of foreign shocks. In theory, a central bank can do everything right. But we don’t live in theory; we live in the real world. The flaw in this argument lies in the impracticality of realizing the ideal central bank for a nation like Argentina. Referring to the behavior of a theoretically perfect central bank is an exercise in the Nirvana Fallacy.

Deputy Luciano Laspina (JxC) employed a familiar excerpt from Milton Friedman (p. 165) in a tweet, citing it to question proponents of dollarization reform.

Dollarization meets Friedman. “If domestic prices were as flexible as exchange rates, it would make little economic difference whether adjustments were caused by changes in exchange rates or by equivalent changes in domestic prices. But this condition is clearly not fulfilled.” pic.twitter.com/X86qfIGh0M

— Luciano Laspina (@LaspinaL) March 30, 2022

Friedman’s passage is not flawed, except that it presupposes a well-behaved central bank, a condition for which no compelling evidence supports in the context of Argentina. Laspina oversees something else: Milton Friedman was one of the first to advocate dollarization for Argentina (see post in Spanish here).

But I digress; let me focus on the two theoretical limitations within this line of reasoning. They are as follows:

Critics should contrast foreign shocks under dollarization with the reality of domestic shocks (caused by inconsistent monetary policy by central banks).

Moreover, some foreign shocks stem indirectly from inconsistent domestic monetary policies - these are not a cost of dollarization.

Furthermore, Calvo (2002, p. 319) asserts that in Latin America, devaluations have mainly led to contraction, and the impact of an external shock can be exacerbated by currency depreciations (owing to dollar-denominated debts). Given that central banks themselves can be sources of substantial shocks, it is not apparent that dollarization is worse than relying on a central bank. This should be evident to anyone with even a modest grasp of Argentina’s economic history.

Empirical Limitations: Whiteboard vs. Data

If dollarization renders a country defenseless against nominal foreign shocks, then it follows that these economies would suffer more significantly than their non-dollarized counterparts. This theoretical "unprotected" dollarized economy is what we envision on the whiteboard. However, does this align with the data? The 2008 crisis constituted an unprecedented shock, implying that dollarized economies should experience an equally unprecedented economic downturn.

Comparing the percentage change in real GDP of three dollarized Latin American countries (Ecuador, El Salvador, and Panama) with Argentina's, we should anticipate a more pronounced decline in the former group. Yet, this is not the case.

Figure 1 shows Argentina’s real GDP contracted by 6.9%, whereas El Salvador's declined by a much milder 2.1%. Conversely, the other two dollarized countries registered positive variations in real GDP. Rather than contracting, their economies slowed—a trend contrary to expectations for a crisis as significant as the one that took place in 2008. Surprisingly (?), this graph contradicts the concerns expressed by critics. This outcome is less surprising if we acknowledge that central banks can mismanage to the extent that their actions inflict more harm than the “straitjacket” of dollarization.

Naturally, a more rigorous analysis would involve regression while accounting for other variables to better gauge how much an external shock impacts a dollarized economy. However, this approach undermines the core of my argument. Given the enormity of the 2008 crisis, any discernible difference should be observable in simple data if critics are indeed justified in their concerns.

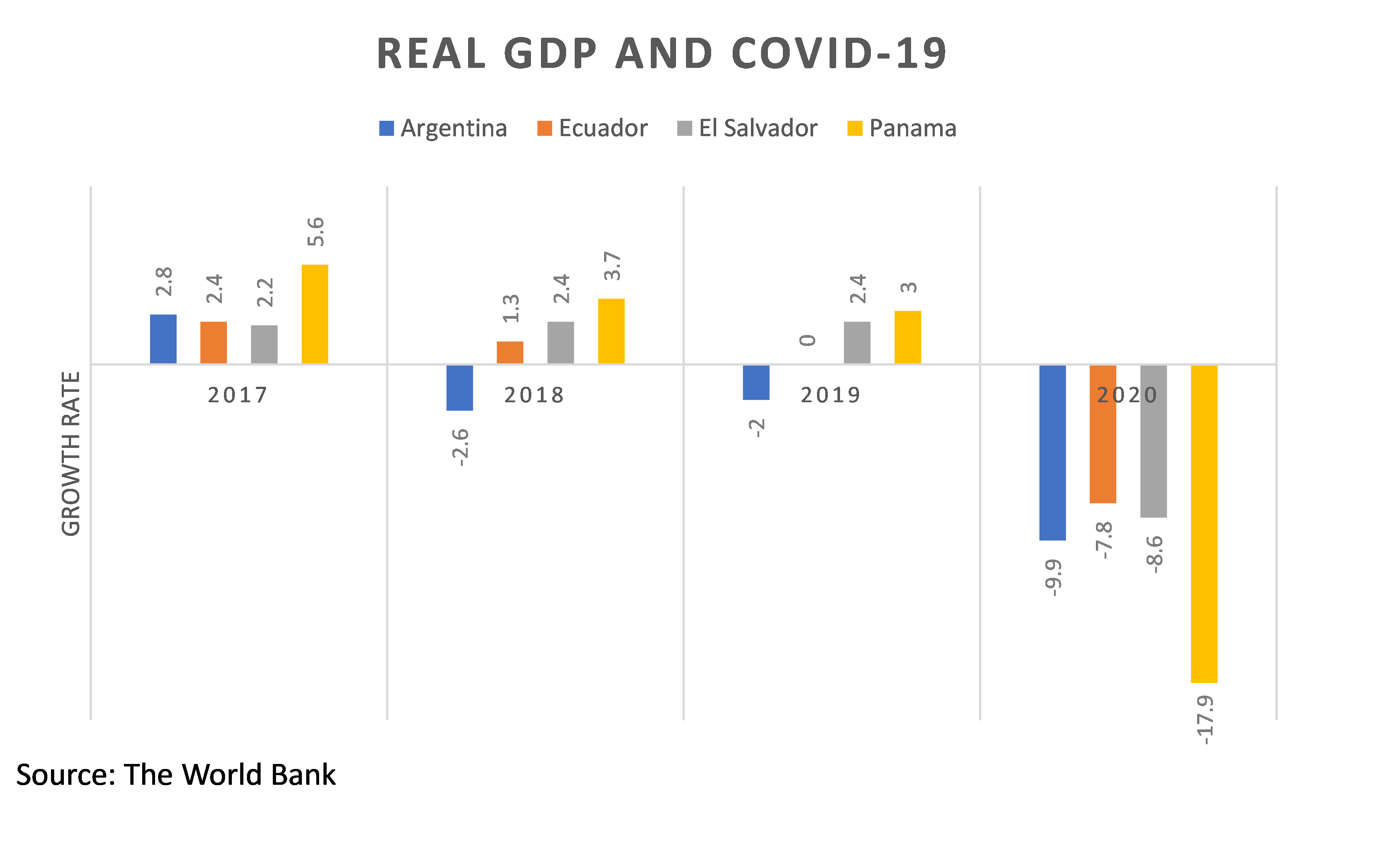

Bonus: Dollarization and Covid-19

What about genuine shocks such as Covid-19? Once more, let's examine the data.

As depicted in Figure 2, except for Panama, dollarized economies suffered less real GDP declines than Argentina. Ecuador not only grappled with COVID-19 but also defaulted on sovereign debt. Nonetheless, Ecuador's economy fared better than Argentina’s. Although all three dollarized economies experienced real GDP drops, they maintained stable price levels in contrast to Argentina, where inflation remains out of control. Furthermore, Panama avoided financial crises or bank runs despite its sharp economic decline, as did Ecuador and El Salvador.

Lastly, it’s crucial to differentiate between real and nominal shocks, as they impact output and inflation differently. A negative nominal shock leads to decreased output and price levels, whereas a negative real shock results in diminished production and higher price levels. Central banks face a dilemma: (1) react to falling GDP, (2) tackle rising inflation, or (3) remain passive.

When facing real shock, monetary policy has limited efficacy. An expansionary approach can mitigate short-term GDP decline at the cost of further inflating prices. Conversely, reducing inflation might deepen the GDP drop. Thus, the reaction of dollarized countries to real shocks is less significant than their response to nominal shocks. Regardless of conclusions drawn from real shocks about the merits of dollarization, the notion that dollarization is unequivocally detrimental seems questionable.

The original Spanish post of this version can be found here.

Next: Dollarization versus currency competition