Loss of Seigniorage is not a Good Reason to not Dollarize

One of the most striking objections against dollarization is the loss of seigniorage, especially in Argentina. For some, the cost of sacrificing seigniorage to achieve lasting price stability seems too high to eliminate the 60% average yearly inflation Argentineans have suffered since the mid-1940s. Let’s delve into the trade-off between dollarization and seigniorage.

What is Seigniorage, and How Important Is It?

Seigniorage is the income generated by the entity issuing the currency. It’s crucial to emphasize that this issuer is often the central bank rather than the government itself. So, when we talk about income to the “issuer” of money, we're not necessarily referring to income for the government.

When a central bank issues money (fiat) that the market demands, it can issue its currency (e.g., pesos) and invest in interest-bearing financial assets. All it has to do is “print banknotes” and use them to purchase these financial assets. The higher the demand for their currency, the more seigniorage the issuer can accumulate.

Now, let’s consider a scenario where the market doesn’t want the local currency, which is currently the case in Argentina. In this situation, the new pesos lead to inflation and currency depreciation. To counter these effects, the issuer must offer incentives, such as paying interest rates (e.g., through instruments like the Leliqs) to maintain demand for pesos.

Now the central bank must pay interest to peso-holders. A low demand for money reduces seigniorage and can even turn it into a negative figure: quasi-fiscal deficit. For example, Emilio Ocampo shows that seigniorage in Argentina hovers around 0.6% to 0.8% of GDP. This figure may not seem a prohibitive loss when compared to Argentina's history of persistent inflation.

Seigniorage and the Inflation Tax

Some individuals may fear losing seigniorage due to concerns about the relevance of the inflation tax. While some authors include the inflationary tax as part of seigniorage, it’s essential to distinguish between the two.

Seigniorage represents the direct income to the money issuer, typically the central bank. In contrast, the inflation tax occurs when the issuer generates money and transfers it directly to the Treasury. As the first recipient, the Treasury obtains “freshly printed notes” that haven’t yet lost their purchasing power. However, due to rising prices, individuals who receive these notes later suffer reduced purchasing power. This dynamic describes the inflationary tax.

To sum it up:

Seigniorage → Central Bank’s income

Inflation Tax → Treasury’s income

In Argentina, seigniorage is limited or negative, while the inflationary tax remains high. This suggests that dollarization has a low cost in terms of seigniorage and offers the benefit of eliminating the inflationary tax.

It's crucial to note that the inflationary tax is:

Regressive (affecting low-income sectors the most)

Highly distorting

Additionally, Argentina’s national constitution prohibits non-legislated taxes like the inflationary tax, as stated in Article 99 (my translation):

Article 99

[…]

The Executive Power may in no case, under penalty of absolute and irremediable nullity, issue provisions of a legislative nature.

Only when exceptional circumstances make it impossible to follow the ordinary procedures provided for by this Constitution for the sanction of laws, and not in the case of rules that regulate criminal, tax, electoral or political party regimes, may decrees be issued for reasons of necessity and urgency, which shall be decided in general agreement of ministers who must endorse them. jointly with the Chief of the Cabinet of Ministers.

Seigniorage Solutions under Dollarization

Beyond the concerns mentioned earlier, it’s important to recognize that seigniorage (income for the issuer) can be addressed under dollarization if the cost of losing this revenue is deemed too high.

Without delving into extensive detail, let’s briefly highlight two points:

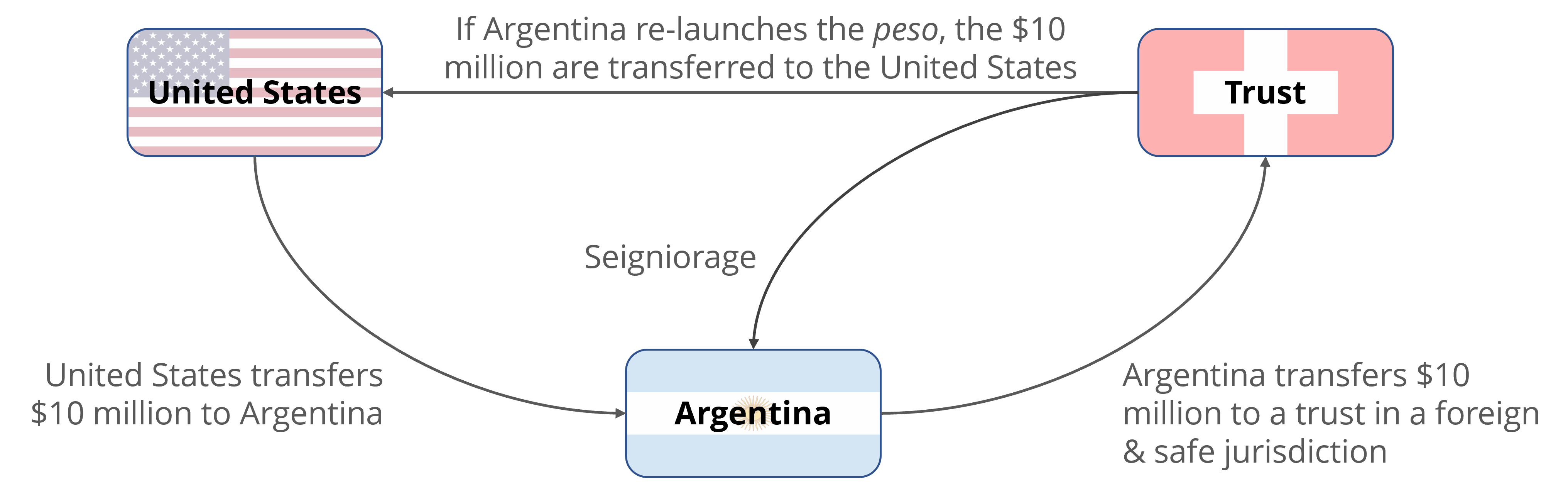

Firstly, a proposal like that of Velde and Veracierto (2000) enables the preservation of seigniorage. Simply put, the Federal Reserve can deposit an amount equivalent to the BCRA's reserves in a secure district (e.g., Switzerland). The income from this fund can then be transferred as seigniorage to Argentina. This trust can be liquidated if Argentina decides to reintroduce its own currency. Because today the Argentine central bank has no net reserves, it has no seigniorage to lose in the first place. The following figure summarizes this proposal assuming Argentina has $10 million in reserves when dollarizing.

Secondly, it’s worth noting that seigniorage is not solely received by the issuer. Commercial banks can also earn a portion of seigniorage by acting as “secondary” money issuers. This can be significant, as Thomas L. Hogan (2012) observed that banks in Hong Kong, Ireland, and Scotland generate hundreds of millions of dollars annually from issuing banknotes.

In conclusion, it’s challenging to view the seigniorage objection as a substantial reason to oppose dollarization in a country that has been struggling for decades to achieve monetary stability. The seigniorage argument appears more as an excuse than a compelling rationale against embracing dollarization.

The original post in Spanish can be found here.

Next: Dollarization versus other Monetary Reforms