Dollarization and Confidence Shocks in Argentina

The Argentine political landscape is often caught in a bind, facing the perennial dilemma of overspending beyond its budgetary limits. Sooner or later, this fiscal recklessness necessitates a reckoning. The aftermath takes the form of soaring inflation (or even hyperinflation), defaults, imposing heavy taxes, or succumbing to exchange rate crises. Essentially, the public sector shifts the burden of its fiscal imbalances onto the private sector.

Over the past 80 years, Argentina has briefly and inadvertently experienced fiscal surpluses, notably after the 2001 crisis. However, these were achieved through defaults and increased taxes rather than a well-thought-out state reform plan. Consequently, it's no surprise that the country swiftly falls back into unsustainable deficit levels.

In essence, the left-leaning populist cycle unfolds as follows [as described by Dornbusch and Edwards (1990)]: A new populist government ramps up spending to unsustainable levels, the inevitable economic deterioration leads to their defeat in presidential elections, and then an “orthodox” administration must undertake the dirty work of fiscal adjustments. This, in turn, fuels discontent among the electorate, prompting them to opt for another populist government and initiating a new cycle of populism.1

Breaking free from this populist cycle demands an austerity plan that avoids an economic downturn and fosters growth. In simpler terms, an austerity plan accompanied by a confidence-inspiring jolt. However, the challenge lies in building long-term credibility when policymakers lack credibility.

Is it possible to carry out an adjustment alongside growth? Empirical evidence suggests it is. One prime example is post-World War II United States.2 In just three years, from 1944 to 1947, public spending as a percentage of GDP plummeted from 45% to 10%. This adjustment didn't result in increased unemployment or reduced consumption.3 The presence of a less intrusive state paved the way for a burgeoning market.

Due to its institutional anomie, Argentina faces numerous hurdles in delivering both a confidence boost and an economic adjustment simultaneously. Cases like Ecuador illustrate that dollarization can import the credibility that local politics struggles to generate. This grants an orthodox government a credibility shock, enabling them to implement adjustments without incurring the political cost associated with economic downturns.

Both Argentina and Ecuador endured parallel economic crises. The 2001 crisis in Argentina led to a staggering 10.9% real GDP decline in 2002. The crisis management serves as a practical guide on how not to conduct fiscal adjustments. In contrast, Ecuador adopted dollarization in January 2001. In the same year, its economy grew by 4%, maintaining positive values until Correa's policies stalled growth in 2015. Meanwhile, Argentina's economy stagnated in 2011, accompanied by high and escalating inflation, setting it apart from Ecuador's price stability.

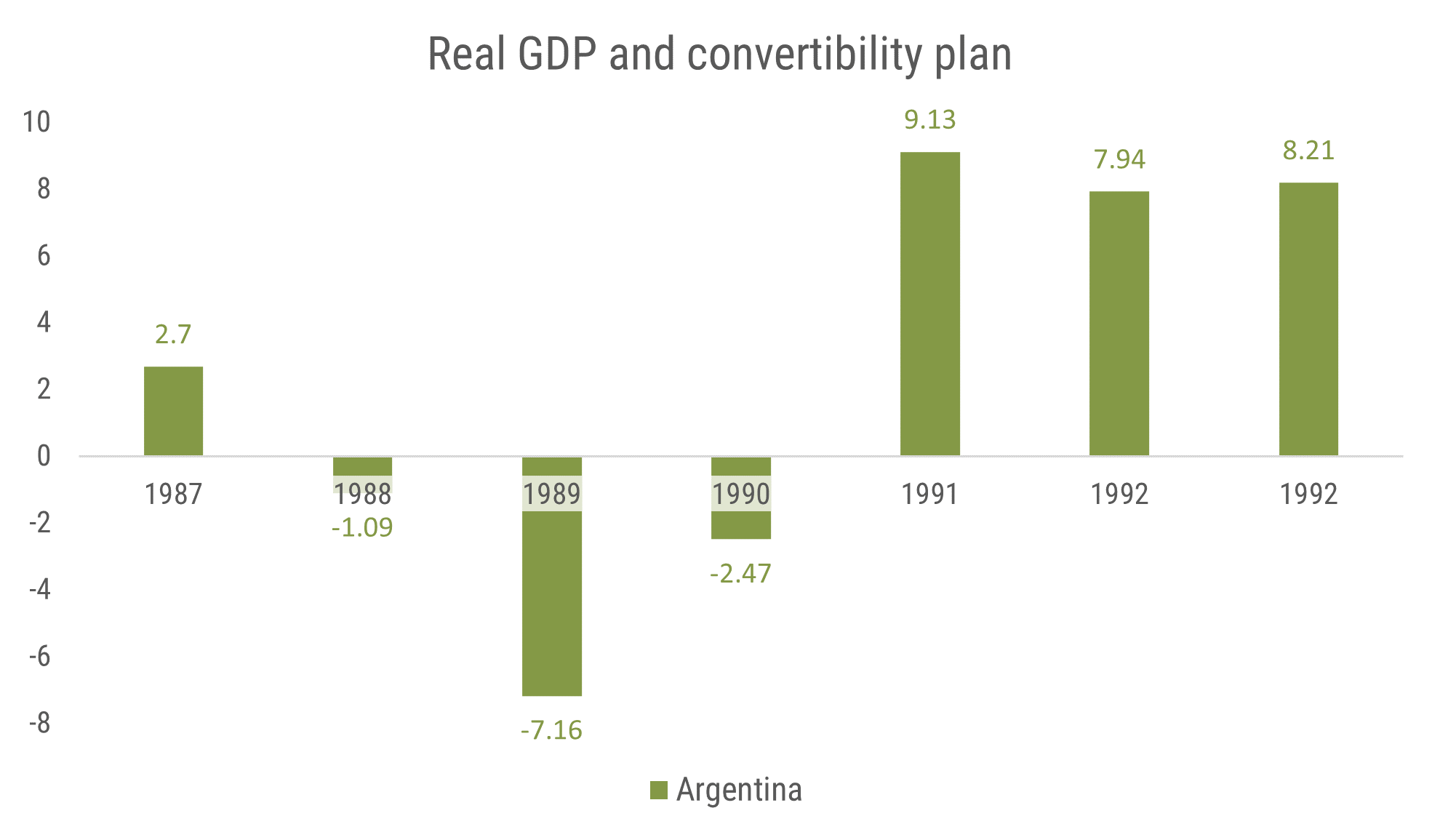

Could Argentina replicate a confidence shock while implementing fiscal adjustments? The case of convertibility suggests it's possible. This strategy swiftly quelled hyperinflation while kickstarting economic growth. In 1989 and 1990, real GDP contracted by 7.2% and 2.5%, respectively. By 1991, real GDP was expanding at a rate of 9.13%.

Unfortunately, this experiment cannot be repeated. By 1991, Argentine society believed that a Congressional law was just that – a law. However, the events of 2001 demonstrated otherwise. The ease with which Congress approved, then revoked, or ignored, laws like zero deficit and deposit protection revealed the lack of credibility in Argentine legislation. The legislative body’s behavior, which has resembled a political instrument since the rise of Kirchnerism in 2003, only exacerbates the credibility deficit. Regardless of the governing party, the legislature is perceived as an extension of the executive branch rather than an independent counterbalance. The legislators are no longer lawmakers but rather “political soldiers” of the incumbent President.

The absence of credibility undermines proposals such as dual monetarism (currency competition) or an independent central bank law. This makes the case for dollarization, as the one Emilio Ocampo and I studied. This approach offers two advantages over other reforms: Firstly, it prevents an economic downturn that could erode the government's political capital, and secondly, it minimizes the risk of failure, averting a mega-crisis that Argentine society is ill-equipped to endure.

Emilio Ocampo (2015) studies the role of commodity prices in Argentina's populist cycle. For my part, together with my colleague Alexandre Padilla (2020) we studied the case for Latin America in general.

For a summary, see David Henderson (2010).

There are some technical details to consider. For example, a series of real U.S. GDP shows a post-World War II decline inconsistent with unemployment and consumption data. The decline in real GDP is not due to a fall in economic activity but to the statistical effect of moving from controlled prices during the war economy to free market prices in 1946. In other words, real GDP was statistically inflated during World War II. This is one of the points Friedman and Schwartz mention in their classic A Monetary History of the United States, 1867 – 1960.

The original Spanish post can be found here.

Next: Dollarization is More than a Fixed Exchange Rate Regime